Weekly Summary: September 27 – October 1, 2021

Key Observations:

- The Delta variant’s effects seem to be more manageable recently, but many supply constraints and disruptions persist.

- Insufficient energy supplies and high energy prices are responsible increasingly for slowing global economic growth and amplifying global inflation.

- We expect that energy related constraints will be more persistent than those caused by the Delta variant.

- The misallocation of resources in China as it becomes more of a “controlled/managed” economy should eventually further exacerbate supply chain disruptions and constraints.

The Upshot: We believe that it could be more difficult to “look through” energy related effects on economic growth and inflation. Same goes for China related policies that focus increasingly on “common prosperity” goals over purely economic growth goals. Global zero carbon emissions policies do not encourage investments that could quickly solve the world’s current energy supply issues. The timing and the extent of any solutions will be very difficult to predict. Global government policies that encourage the development of “renewable” sources of energy will continue to be very uncertain as to when tangible results that would help solve many of our energy issues will be forthcoming. We expect that China’s increasing regulations and scrutiny over its economy could become more unpredictable in terms of their content and timing.

Delta Variant Effects Subsiding

As we described in our latest weekly commentary dated September 24, the Federal Reserve (Fed) appears to be “all in” with respect to looking past the Delta variant’s effects on inflation and employment/economic growth. There have been many indications that Delta-variant-related infection rates are declining. One such example found in a Boston Globe September 29 report, indicated that the seven-day moving average of new infections in the U.S. has fallen from approximately 160,000 at the beginning of September to just over 110,000 as of September 27. Other infection rates measures for September have also shown a lower trend of infections in 47 states, as well as Washington D.C.

Global Economic Momentum Slows

However, the Delta variant’s effects still continue to slow global economic momentum. The flash (preliminary) Purchasing Managers’ Indexes (PMIs), based on surveys of senior executives at private sector companies conducted by IHS Markit and announced last week for the U.S., Eurozone, U.K. and Japan, all indicated slower economic growth rates and rising prices for September. PMI is an index of prevailing economic trends in the manufacturing and service sectors. The IHS Markit September 24 report noted that in general, price increases accelerated at the second highest rate in the series’ eleven-year history. Most input costs increases were attributable to growing material shortages and supply chain constraints. Meanwhile, manufacturing growth slowed to its weakest rate in about a year and service sector growth slowed to a level not seen since February. In other words, as J.P. Morgan’s (JPM) “Eye on the Market” highlights in its report of September 27, supply chain problems are not getting better as economic growth momentum slows. Similar conclusions could be drawn from surveys conducted in September by the Federal Reserve Banks of Richmond and Dallas, whose results were published this week.

Supply Constraints Persist

Even as the incidence of coronavirus infections were decreasing and many economies were in the process of reopening, supply constraints continued to hamper economic growth rates. As indicated in the previously cited Eye on the Market report, the semiconductor shortage might persist into Q2 2022. This chip shortage will affect especially the automobile industry, because of long lead times needed to increase production.

Shipping delays and shipping price distortions are also expected to constrain needed input supplies. The much higher eastbound freight shipping rates (from China to the U.S.) as compared to the westbound rates are such that incentives were created for ship container owners to send their containers empty back to China to accelerate receipt of more eastbound freight rates. This is an example of how shipping distortions could lead to more supply chain disruptions.

U.S. Consumer Confidence Dampens

The Conference Board’s Consumer Confidence Index released on September 28, indicated that a slowing rate of economic growth accompanied by increasing prices continued to dampen U.S. consumers’ confidence in September. Both on an assessment of current business conditions and ln their short-term outlook, the Delta variant’s effect was very evident on consumer optimism. The Senior Director of Economic indicators at the Conference Board revealed that spending intentions for homes, autos and major appliances all retreated. Furthermore, although concerns eased somewhat, short-term inflation worries remained elevated. Consumer confidence remained high enough, however, to support higher spending in the short term. Since consumer confidence also declined in July and August, the Senior Director thought that these declines, taken together, “suggest consumers have grown more cautious and are likely to curtail spending going forward.” Moreover, when prices increase to certain levels “demand destruction” is also possible.

EU Confidence Rises as Delta Variant Contained

In contrast to the U.S., consumers in France and Germany appear to be feeling more confident in September. According to a Citi Research report from September 28, consumer confidence in France hit a three-month high that month. Despite rising inflation worries, partly due to surging natural gas prices in Europe, the French consumer focused more on the continued fall in COVID-!9 cases and the “smooth back to school period.” The possible medium-term hit to their purchasing power due to higher energy costs could not overcome the rise in consumer confidence. Similarly, the German consumers’ economic and income expectations improved sharply in September, even as higher prices weighed on their purchasing intentions.

Surging EU Natural Gas Prices

In fact, Citi expects natural gas and electricity prices to rise another 10% in Germany during the upcoming winter season. Less wind-generated power in Europe due to less windy conditions also contributed to a higher demand for natural gas, which translated to higher prices for natural gas. In a report also dated September 28, Goldman Sachs noted the recent substantial increase in European natural gas prices is further pressuring input costs, as well as fueling inflation and slowing the economic growth in Europe (EU). The recent surge in EU natural gas prices, the curtailment of output characterized by global supply chain disruptions, higher input costs due to component shortages and higher shipping costs and delays, all contributed to Goldman’s downgrades of its global GDP forecasts, especially for Q3.

Insufficient Energy Supplies

Insufficient energy supplies and high energy prices are increasingly affecting production outputs of many types of goods. Supply chain disruptions could become typical byproducts of insufficient and highly priced energy. High natural gas prices are beginning to have such an effect in Europe. Supply issues are becoming more prevalent in the U.K. due to more idiosyncratic issues. The U.K. withdrawal from the European Union has prevented many immigrants from working in the U.K. This has led to a critical shortage of truck drivers within its borders. Additionally, the pandemic prevented the timely processing of truck driver licensing applications. The most prominently reported U.K. shortage this week was the main reason for the dearth of gasoline deliveries to petrol stations. Lack of gasoline supplies has caused great supply chain strain this week and has slowed U.K. economic growth.

China Energy Issues

Energy issues in China are causing supply chain disruptions and are negatively impacting production. Although first introduced in China’s 5-year plan of 2005-2010, the “dual control system” was recently made very specific. This system which has the dual goal of limiting energy consumption overall and the energy intensity used in various industries, is part of China’s longer term goal to reach peak carbon emissions by 2030 and carbon neutrality by 2060. In mid-September, China’s National Development and Reform Commission (NDRC) intensified its efforts to control levels of allowable energy consumption and intensity at the province level. The August NDRC report classified provinces according to whether they had achieved the targeted levels of energy usage. The NDRC also added extra incentives to comply with the targeted levels of electricity usage. For example, missing targets may lead to delays or suspensions in NDRC’s approvals of new energy projects for localities.

According to a Goldman Sachs September 28 report, the pandemic has made China’s economy at least temporarily more energy intensive, which affected especially its manufacturers focused on exports. The industrial manufacturing sector accounted for about two-thirds (67%) of China’s total power consumption in 2020 compared to approximately 16% attributable to services.

Electricity Rationing in China

A September 30 Citi Research report highlighted that over 20 provinces, which make up more than two-thirds of China’s GDP, have implemented electricity-rationing measures since August. This power rationing has disrupted supply chains and has led to the curtailment of production in some industries, as well as price increases. China’s recent electricity supply shortage is also due to its power sources. Thermal power (73% of total power production in 1H) has become more limited recently due to low supply and surging prices of coal. The coal shortage was partly self-inflicted. China cut drastically its coal imports from Australia earlier this year. Consequently, China’s coal prices have nearly doubled in 2021 and are more than 50% higher just in September.

Citi’s September 30 report observed that many provinces failed to meet NDRC’s electricity usage targets as revealed by NDRC’s report released on August 17. “This led to a series of factory shutdowns and production cuts in energy-intensive and high emissions sectors.” Sectors especially hard hit by the electricity cutbacks included steel, non-ferrous metals, cement, glass, coking, chemicals, industrial silicon, paper making and electroplating.

In a further showing of its “command” economy, the Chinese government has prioritized household electricity use (14.5% of total consumption) over industrial use. The government might limit further production of raw materials in northern China to slash pollution in an effort to ensure blue skies for Beijing’s upcoming Winter Olympics. Production controls are set to continue at least until Q1 of next year.

Source – Citi, China Economic: Power Outages Strengthen the Case for (Short-Term) ‘Stagflation’ (9/30/2021)

Stagflation?

It is possible that all of these cutbacks and shortages could even lead to a short-term period of stagflation in China, and perhaps elsewhere as well. As we have previously highlighted, China would then become an exporter of inflation. Global inflation and slower economic growth would also be exacerbated by China’s supply constraints and disruptions. These are the types of concerns that have led many Wall Street firms to downgrade their global GDP growth forecasts for this quarter as well as Q4 and for next year.

China’s Manufacturing PMIs Show Contraction

China’s rising stagflation risk was reinforced by the release of its weaker than expected manufacturing PMI for September, that overall dropped below 50. A below-50 reading signifies a contraction in manufacturing. The larger firms continued to outpace the smaller firms. According to another September 30 Citi report that focused on China’s PMIs, the production index declined by a “significant” 1.4% to 49.5. “The abrupt power cuts and the ‘dual energy control’ already started to show the impact.” Purchasing price and producer prices continued to rise, as the energy outages and supply disruptions kept up industrial prices.

Source – Citi, China Economics: Contractionary PMI Points to Rising Stagflation Risk (9/30/2021)

China’s Services PMI Shows Delta Variant Contained

Surprisingly, China’s non-manufacturing PMI almost completely reversed its severe August fall to below 50 and has risen above 50 once again in September. The services PMI returned almost to its pre-Delta variant level, as the still expansionary construction sector decreased, which is likely due to the property sector slowdown. Evidently, China has largely been able to contain the Delta variant.

China’s Managed/Controlled Economy

As the above discussion enumerates, China’s government has recently become even more controlling in determining the winners and losers in its economy. China also is now promoting its “common prosperity” goals. It appears that China’s social and political goals are superseding even its economic growth objectives. As China’s economy becomes even more of a “control/managed” economy, we anticipate that supply disruptions and constraints will only increase. There are simply too many interrelationships among products, economies, industries, etc. for a central authority to efficiently allocate its resources.

Energy Related Supply Constraints and Disruptions

Energy-related constraints appear to be increasingly responsible for a global slowing of economic growth and a more persistently high level of inflation. Our expectation of USD weakening in the intermediate term was predicated on economic growth of selected foreign countries “catching up” to U.S. economic growth once the Delta variants infection rates subsided and their economies reopened. We anticipated that a “rolling economic expansion” would eventually weaken the USD and would prolong positive economic growth. It now appears to us that energy-related dislocations could further delay economic recoveries of many countries. This confluence of events could further delay the USD’s eventual depreciation. But to the extent that USD remains buoyant, it will help contain U.S. inflation, but it will hurt commodity prices and make foreign holdings and earning marginally less attractive. All of these factors — except USD strength — should continue to result in more persistent and higher rates of inflation. Everything else being equal, we continue to expect higher interest rates in the intermediate-term.

We expect that energy related shortages might continue for an extended period. China is only one of many countries with goals to achieve zero-carbon emissions goals. Global government policies mostly support investments in renewable energy technologies. Fossil fuel investments are generally discouraged. Given these policies, many investors will be reluctant to invest in projects that would quickly solve some energy supply issues.

Bottom Line

Just as the Delta variant was becoming more manageable and contained and the reopening of economies were about to re-accelerate, it has become more evident that energy related constraints and disruptions could inhibit global economic growth and exacerbate inflationary pressures. But unlike the Delta variant infections that especially hurt the services part of economies, we expect that the energy related supply disruptions will be much more focused on the manufacturing and production part of the economy. As a consequence of this focus, we believe that energy related issues will have much less of an impact on U.S. employment when compared to the Delta variant. China’s latest PMIs for September generally corroborate this thesis.

Because of its more negligible impact on U.S. employment, we don’t believe that energy related issues that disrupt or constrain supply chains will affect the timing of the Fed’s tapering timetable or its contemplated “liftoff” – when the Fed will begin raising interest rates. We continue to expect that the Fed will announce its decision to begin tapering at its November 2-3 meeting and will actually begin to taper in mid-November, when it usually makes its monthly purchases of securities. If anything, a more persistent and higher level of inflation might even lead the Fed to accelerate its timetable of reining in its “easy” monetary policies.

Energy related issues as we have described them, most likely will delay our “rolling economic growth” scenario where economic growth would first peak in China, to be followed by the U.S., EU, emerging markets (EMs), etc. Such a scenario would have prolonged the economic growth cycle and we believe would have produced a lower USD trajectory. We still believe that the next major move in USD over the intermediate term will be lower from its current near 52-week high as the economies of foreign countries play “catch up” with the U.S. We also continue to expect that interest rates will trend higher over the intermediate term, but perhaps in an irregular manner.

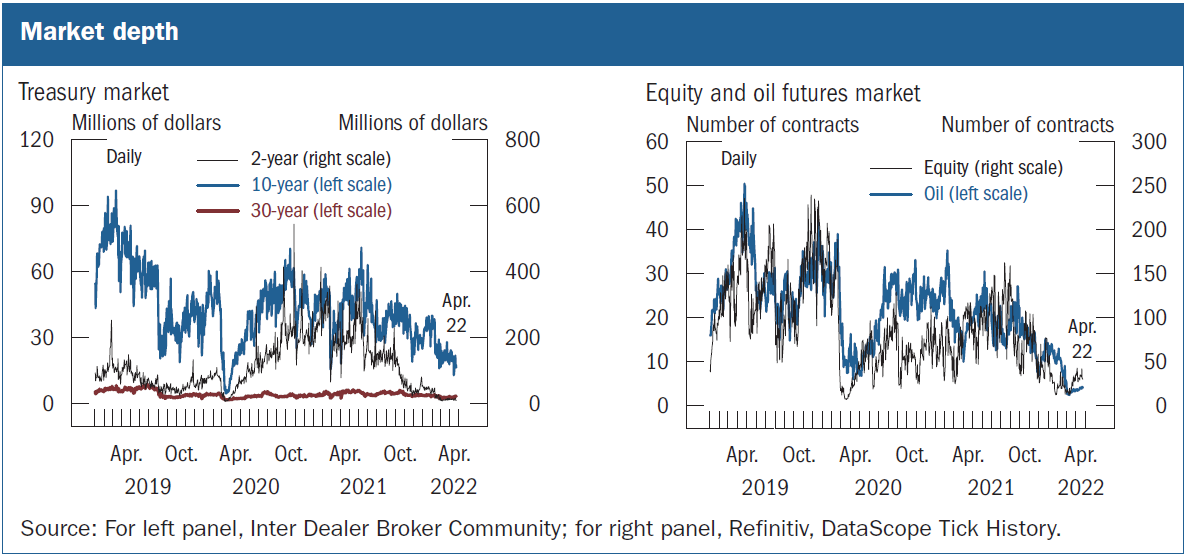

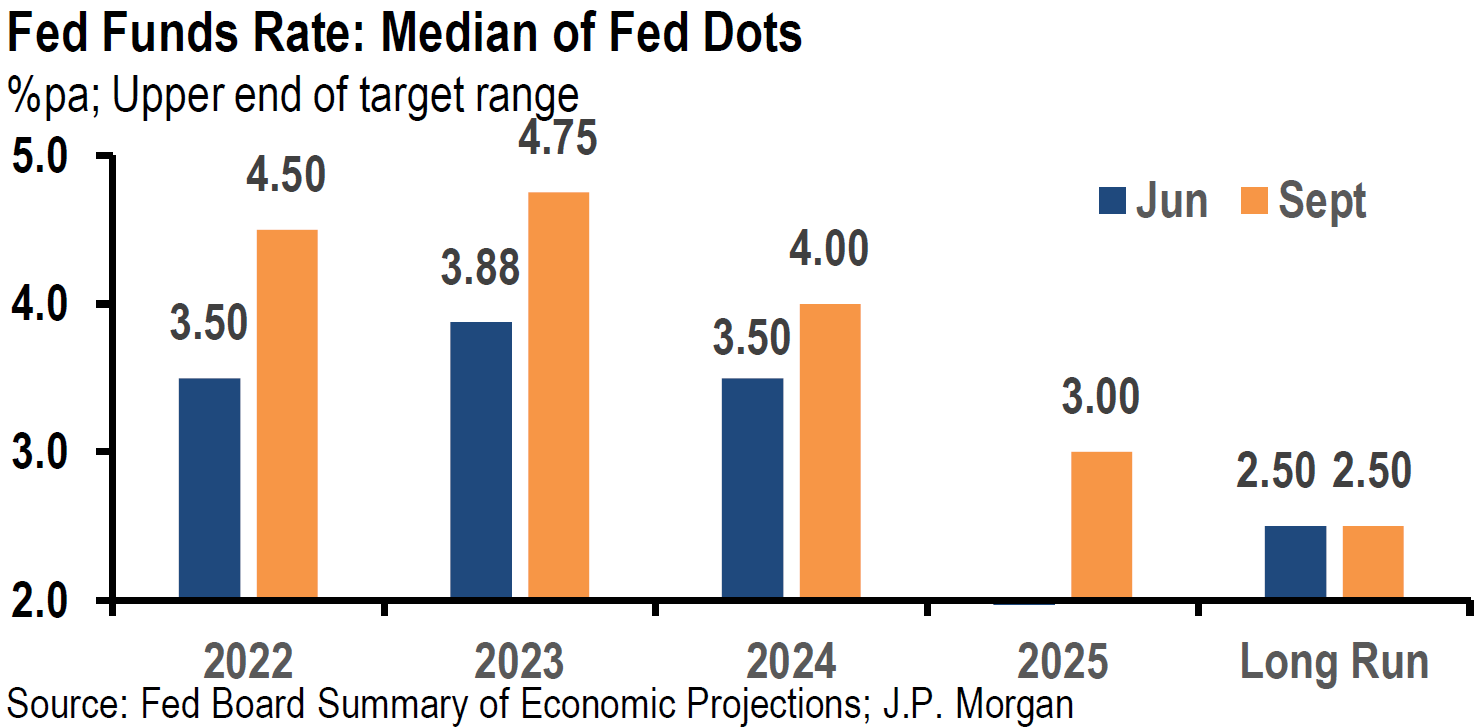

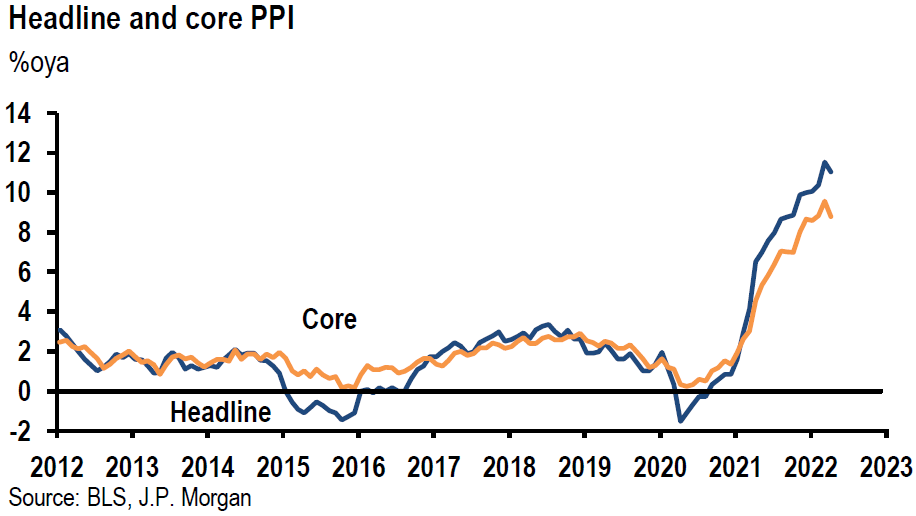

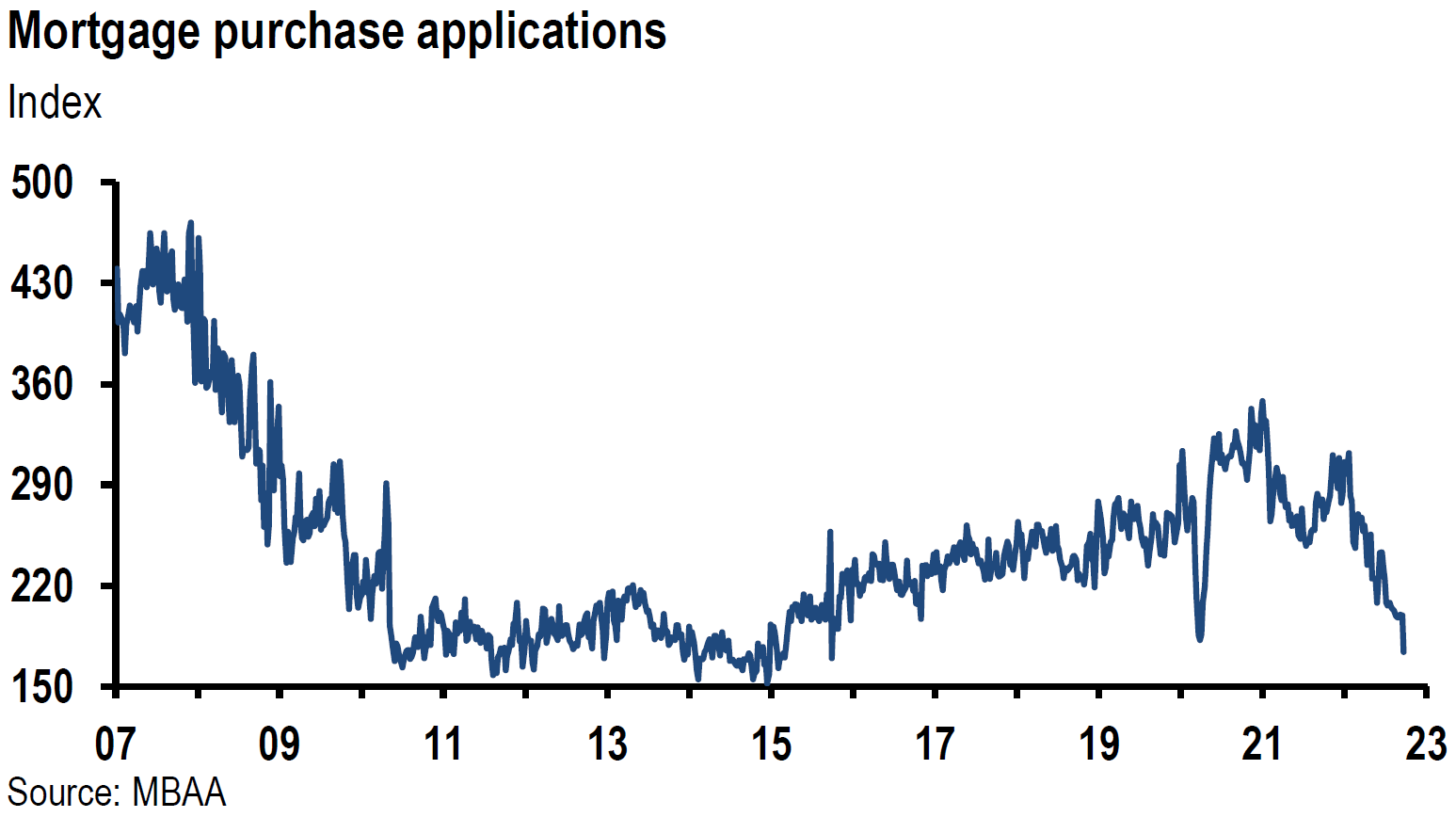

Charts of Interest

Source (left) – J.P. Morgan, US Weekly Prospects (9/24/2021)

Source (right) – J.P. Morgan, The J.P. Morgan View: Markets to continue following the path of COVID recovery (9/27/2021)

Source – Citi, Global Economics Weekly: Who Is Vulnerable to a Chinese Slowdown? (10/01/2021)

INDEX DEFINITIONS

KBW Nasdaq Bank Index (BKX): The KBW Bank Index is designed to track the performance of the leading banks and thrifts that are publicly-traded in the U.S. The Index includes 24 banking stocks representing the large U.S. national money centers, regional banks and thrift institutions.

MSCI EM Value Index: The MSCI Emerging Markets Value Index captures large and mid cap securities exhibiting overall value style characteristics across 27 Emerging Markets (EM) countries.

MSCI EM Index: The MSCI Emerging Markets Index captures large and mid cap representation across 27 Emerging Markets (EM) countries.

NASDAQ: The Nasdaq Composite Index is the market capitalization-weighted index of over 2,500 common equities listed on the Nasdaq stock exchange.

PCE: Personal Consumption Expenditures (PCEs) refers to a measure of imputed household expenditures defined for a period of time.

Russell 1000 Growth: The Russell 1000 Growth Index measures the performance of the large-cap growth segment of the U.S. equity universe. It includes those Russell 1000 companies with higher price-to-book ratios and higher forecasted and historical growth values.

Russell 1000 Value: The Russell 1000 Value Index measures the performance of the large-cap value segment of the U.S. equity universe. It includes those Russell 1000 companies with lower price-to-book ratios and lower expected and historical growth rates.

S&P 500: The S&P 500 Index, or the Standard & Poor’s 500 Index, is a market-capitalization-weighted index of the 500 largest publicly-traded companies in the U.S.

VIX: The VIX Index is a calculation designed to produce a measure of constant, 30-day expected volatility of the U.S. stock market, derived from real-time, mid-quote prices of S&P 500® Index (SPX℠) call and put options.

Z-Score: A Z-score (also called a standard score) gives an idea of how far from the mean a data point is. It is a measure of how many standard deviations below or above the population mean a raw score is.

IMPORTANT DISCLOSURES

The views and opinions included in these materials belong to their author and do not necessarily reflect the views and opinions of NewEdge Capital Group, LLC.

This information is general in nature and has been prepared solely for informational and educational purposes and does not constitute an offer or a recommendation to buy or sell any particular security or to adopt any specific investment strategy.

NewEdge and its affiliates do not render advice on legal, tax and/or tax accounting matters. You should consult your personal tax and/or legal advisor to learn about any potential tax or other implications that may result from acting on a particular recommendation.

The trademarks and service marks contained herein are the property of their respective owners. Unless otherwise specifically indicated, all information with respect to any third party not affiliated with NewEdge has been provided by, and is the sole responsibility of, such third party and has not been independently verified by NewEdge, its affiliates or any other independent third party. No representation is given with respect to its accuracy or completeness, and such information and opinions may change without notice.

Investing involves risk, including possible loss of principal. Past performance is no guarantee of future results.

Any forward-looking statements or forecasts are based on assumptions and actual results are expected to vary from any such statements or forecasts. No assurance can be given that investment objectives or target returns will be achieved. Future returns may be higher or lower than the estimates presented herein.

An investment cannot be made directly in an index. Indices are unmanaged and have no fees or expenses. You can obtain information about many indices online at a variety of sources including: https://www.sec.gov/fast-answers/answersindiceshtm.html or http://www.nasdaq.com/reference/index-descriptions.aspx.

All data is subject to change without notice.

© 2021 NewEdge Capital Group, LLC